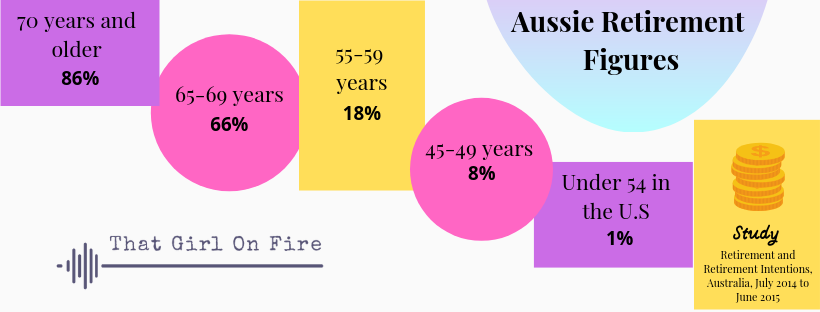

My Financial Independence, Retire Early (FIRE) journey began when I was a little girl. I would look at people working until they were in their 70’s, mostly when they didn’t want to, and feel so bleak about my own working future.

Still, everywhere I turned, working was a necessity, because there was no other alternative. Even more strangely, working until old age was just something that was expected.

This I didn’t understand… surely there were more interesting ways to collectively spend our precious time? And why would we choose to work until we could barely stand anymore?

It wasn’t until I was in the workforce myself many years later that these feelings became particularly profound.

Despite my earnest excitement to be earning a full-time wage (9.5% superannuation! Annual leave!), I couldn’t shake the thought that working until 70 was now the bottom-line of my life.

Sure, I might get lucky and always enjoy my roles – and in a hopeful economy, the income would be consistent and well worth what I spent on my university degree.

Still, I’d be in it for the long-haul because that was just what humans had to do at this point in history.

To be honest, it really grated at me. I felt hopeless for a while.

Then I found FIRE, and I symbolically danced around it like the early homosapiens did a million years ago.

FIRE stands for Financial Independence, Retire Early; a term encompassing a whole community of people who were architecting amazing lives without the need for exchanging their time for a steady income.

This was the money-savvy elite; the personal finance prefects, who saved aggressively and invested it with as much fervour. In mere years, they had created income streams that were entirely passive.

Passive income, retire early def: “Passive income is income resulting from cash flow received on a regular basis, requiring minimal to no effort by the recipient to maintain it.” – Wikipedia.

In many cases, this passive income replaced (and sometimes exceeded) their day-to-day pay check.

It was through anything from share market dividends, rental yield, retirement fund payouts, interest payments from bonds and term deposits and even ad revenue or royalties from content.

Whether it was one, two, or all – the underlying outcome was the same:

Work was optional.

I’d always been okay with my money. I saved when I could, I stayed away from toxic personal debt and tried to live within my income bracket – but this was going to require a lot more dedication. I was committed and started straightaway.

Over the last 8 years, my husband I have saved over half a million Aussie dollars combined, pouring our earnings into investments that will buy our retire early “work freedom” decades before we otherwise could.

Now, we routinely invest 75% (or more) of our incomes each month into a very strategic investment portfolio across property, shares and stocks, superannuation, commodities and bonds.

We’ve seen some awesome returns so far and it’s spurred us to keep going.

Our (conservative) calculations show that we should be completely financially independent from our jobs at some point within the next decade.

These calculations take into account inflation (of which our investment returns should easily exceed) and any taxation implications. They also factor in the average cost of having and raising a child. We are trying to cover every base.

This isn’t by any means a definitive list, but it gives you a snapshot of the principles behind how we do what we do.

Live for the income you earn, not the income you want.

It’s money management 101, but it bears repeating – especially in this day and age.

While it’s never been more normal to self-deprecate and and laugh at our own misgivings, we’re also living in an age of total social fabrication. The Keeping Up With The Joneses mentality has transcended our immediate neighbourly boundaries and landed smack bang into our virtual ones.

We see highly-stylised lifestyle snapshots for people living in all corners of the globe. It looks effortless and abundant and we struggle to discern between what is product placement and what is truth.

Marketers are insidious; they find us anywhere and everywhere and will stop at nothing to make cart checkouts easier, fuller and more recurring. Loan providers are predatory and advantageous.

But we also have a responsibility to start spending more dutifully, too. When a 2018 survey of household comfort found that 1 in 10 Australian households overspent their income each month (with less than $1000 in savings to accommodate the shortfall), it was obvious where a lot of the culpability was lying.

Get to know every dollar coming in, and be ruthless in every dollar going out. Use a budget to account for important, non-negotiable costs, and eliminate anything that’s draining your money.

When income does rise, be careful not to inflate your lifestyle costs to go with it. My income varies as a small business, but my expenses do not. That means extra profit goes straight into investments. As for any loss? It barely touches the sides of my cost of living.

For those new to the retire early lifestyle, it might be easier to start with a very conservative savings rate of 10%. When this starts to become habitual (and easier), ramp it up.

Want to retire early? Have less in order to do more.

Being thoughtful, intentional and premeditated in the way you allow material things to come into your life is a very important pillar of financial independence. Granted, not everyone who subscribes to the FIRE methodology is a minimalist – but I think the most successful ones are.

The name of the game is personal abundance: finding joy in experiences over objects, and using the space created by decluttering to make way for more enriching pursuits.

For me, cutting out the consumer noise led to a greater appreciation for so much more beyond the stuff.

Not only did I make money in what I could sell, but I save so much in only buying what I need, when I need it.

I do not allow marketers to incessantly bombard me, I never kill time by meandering around the shops, and when I identify something I do need to buy, I compare widely and pay using cash for discounts (I also use cash-back apps).

If it’s true that we overspend or impulse buy because we’re overwhelmed, time-poor and exhausted, then it stands to reason that eliminating or streamlining these triggers will do us a world of personal and financial good.

Start investing, and then do not stop.

Generally speaking, the average return of the sharemarket is about 7% (this has been even despite major economical dips and world events).

Other investments can do equally well (if not amazingly well) but are typically a little more dependent on other factors (for example, geography and uniqueness in the case of property).

I won’t list these all here because there’s no one-size-fits-all approach to investing – but, if you invest sensibly with the goal to make long-term return, the outcome will rarely be bad.

Long-term return really is that which is focused on growth (growing in value over time), and providing cashflow that exceeds the rate of inflation. Savings accounts don’t always do this – and sometimes you can even go backwards with your money “invested” through the bank.

Investing in high-growth investment vehicles with a moderate amount of risk is where a lot of retire early proponents carve their path. It’s certainly where we’re carving ours.

We learnt how to invest ourselves by reading widely, attending talks, speaking to financial professionals, and a little trial and error. It’s completely possible to invest well on your own (just like it’s completely possible to invest well with expert help).

It depends on the person and situation.

Our investment portfolio is a mix of property, shares (mainly Australian and US exchange-traded funds but some individual companies and classes), superannuation, and a few others. They’re in liquid and non-liquid vehicles – meaning we could pull out money in some without much hassle, and others with a lot.

But, we don’t really plan on doing that. Why? Because these investments are going to provide the brunt of our income one day.

In the future, we’re keen to start investing seed capital in startups, which represents a much higher risk. This is because I believe people and ideas drive successful shareholder returns, and I want to be at the forefront of finding great investments this way.

I also like having diversity across the type of investments we have (this makes it easier to weather the storm during market fluctuations).

Ultimately, how and where you invest is up to you. But start ASAP. I talk about this on my Instagram sometimes; how people often wait for ‘market drops’ and ‘share sales’. This is great if you can buy on sale (in fact, it’s my favourite time to buy), but if you haven’t yet invested… you probably don’t know what shares on sale look like.

And you won’t until you’ve had some time in the market, observing how it works. The best thing to do is to start.

Build an emergency fund that keeps you afloat.

Although savings accounts aren’t always great for investing potential, there’s certainly a place for them – at least in our journey.

In FIRE (and in everyday life), cashflow is so important. In particular, having access to money stored away that prevents you from reaching for lines of credit or putting yourself in compromising financial positions can make or break your efforts.

We call ours our ‘S*!# Happens’ account, and it makes up about six to eight months worth of our combined yearly expenses. We use it to cover unexpected bills and curveballs we didn’t anticipate, as well as act as a buffer in case one of us can’t work for a period of time.

The reason cashflow is important is because it keeps you liquid without penalty.

While it’s important to have some liquid investment assets, there’s no guarantee the market will be performing well when you want to draw them. Plus, there’s that pesky capital gains tax that might apply to the sale.

Having access to cold, hard cash bulletproofs you against the unexpected, and it keeps you afloat when you need it the most. It’s very powerful for your wallet and your sanity, and a high-interest savings account (with no withdrawal penalties) can at least earn you a little while it sits there.

We employ our savings to offset the interest applied to our principal mortgage, which for us far surpasses the return of a savings account, but it depends on your unique situation.

We invest first, save second, pay routine expenses third and spend last – this is a good formula to follow when it comes to saving your own emergency fund.

If you’re in debt, think about swapping out the investing part with paying down debt until you’re ready for that step.

Live to give.

This one is worth mentioning because it’s the right thing to do upon amassing more wealth.

When you start to get better with money, think about how you can better the lives of others with your changes. After all, the secret to living is giving.

Not only can it be super tax-effective, but it a core pillar of how many retire early followers plan to contribute to the world in absence of their work (should they choose not to work on anything).

The amazing thing about FIRE is that people don’t have to have great money stories to start doing it.

In fact, some of the FIRE followers who adopted the FIRE principles didn’t do it to retire early – but to speed up their journey away from stagnant debt. They did it to become more financially free. Often, just like us, they were everyday earners.

We’re not expecting a major inheritance or paying for everyday expenses with a trust fund.

While we earn good incomes, they are still commensurate with that of those expected in a major capital city. We have higher expenses for that reason, too.

We chuckle at times about how when we reach complete FIRE, we might choose we aren’t ready to retire early at all.

I enjoy running my business and he finds his work very rewarding – but that’s the amazing thing about the Financial Independence, Retire Early movement.

When something is based on opportunity, it’s hard not to start thinking about what you could do with all of the new open doors.