A lot of folk say that financial independence doesn’t follow a linear path. That the stages of financial independence change.

I disagree, because actually, if you look at common themes in people’s finances across the spectrum, the trends are clear.

Personal finance is of course, always personal, but the “stage” we find ourselves in at any point in our life is often one of only five others. This starts at being completely dependent on others and ends at being completely financially independent from anyone.

Everything in between is where you make your money mojo.

Bear in mind, some people never move out of the first couple of stages, or sit comfortably somewhere in the middle anticipating a traditional retirement at 65. Some people get to the later stages, but fall back after major life catastrophes, and a small handful reach the holy-grail state of eternal passive income and are financially set for life.

Whatever your current stage, it’s not too late to progress it. Once you understand where you sit, the reality sinks in and you can start looking at where you want to be, moving out of the stage that doesn’t suit and into one that looks a bit better on you. Here are the stages of financial independence, from dependence to abundance, surviving to thriving.

Stage 0 – Dependence

Baby, you were born this way. This is what I’d call the newborn state, where your basic existence is funded by others – their financial generosity feeds you, clothes you, keeps you warm and well and covers your everyday needs. This is usually your parents, or carer – but shockingly, adults also fall into this category. It’s called debt; a lifestyle funded entirely by creditors, where you spend more than you earn and your income (if any) barely touches the repayments. If that life line was cut off, you’d sink.

Stage 1 – Solvency

The next in the stages of financial independence is called solvency, where you’re up-to-date on your bills and meeting your financial obligations as and when they come in. You don’t depend on handouts or credit, you’re not creating anymore debt with your lifestyle choices and by all accounts, you’re earning some sort of profit through your income – you’ve got some disposable cash. If you’re actively paying down debt – even if it’s a minimum repayment – you are paying down your bills so you are considered solvent (amazing work – this is the first step to building real, lifelong wealth).

Stage 2 – Stability

Stability is achieved once you’ve hit some basic financial goals – like being personally debt-free. Note that this is debt outside of that which is typically considered to have growth potential, like a mortgage, a business loan or student debt (this is still a priority to pay off but not as urgent as consumer debt). And if you’ve got some basic savings to cover an unexpected event, as well as continuing to support yourself with your income, you’re stable.

Stage 3 – Agency

You’re completely debt free! Congratulations. This is one of the most important stages of financial independence. You’ve paid off all debt, including a principle mortgage and you’ve got enough FU Money in the bank to walk away from anything at any time (my advice is to have this in your arsenal, anyway). You’re a free agent, not tied to anyone or any workplace entity to dictate your decisions. This is the last stage in the “surviving” category – from here, it’s all about building wealth. In my humble opinion, you can (and should) start this building wealth ASAP. It’s never too early to start investing.

Stage 4 – Security

So you’ve been diligently investing in a broad range of asset classes and now, your passive investment income (income you do not actively work for) covers a basic standard of living. Simple food, keeping that roof over your head (either rent, or because you’ve paid off your mortgage like in the third stage of financial independence – covers basic fixtures, repairs and annual home and contents). Maybe also medical expenses, new clothes when the old ones tatter, the bus fare to town. Not much more, but you could do this indefinitely.

Stage 5 – Independence

Those magical words – financial independence. This is where the standard of living you’ve become accustomed to, and those creature comforts you love, are both serviced by your investment income. You don’t need to work if you don’t want to. You’re living well above the poverty line in a modest and comfortable but fulfilling way. As you’ve probably been investing for a while, this way of life is not new and something you’ve grown happily accustomed to.

Stage 6 – Abundance

Although I write a lot about financial independence – financial abundance is really the goal with money, at least for us. Your passive income pays for everything, and then some… you can travel, build a passion business (with no expectation or need for it to become profitable), you can give wealth away to others, you can make guilt-free luxury purchases… the list is endless. You’re earning far more than you need so a huge chunk of that income is disposable. Ah-mazing!

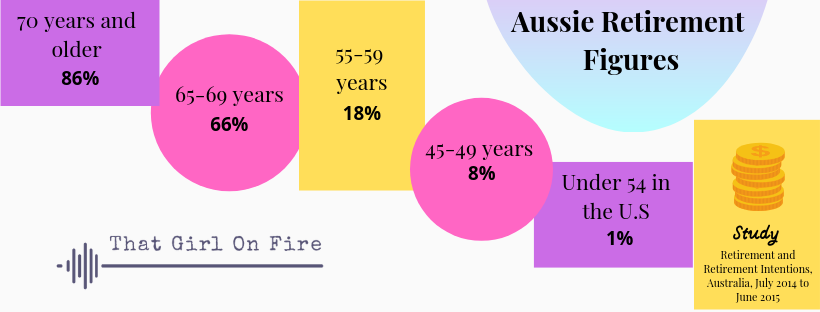

How young can we achieve this? According to a U.S. LIMRA Secure Retirement Institute study, less than 1% of people will achieve retirement before the age of 54. Closer to home (ABS research), 8% will achieve it between the ages of 45-49 years, with presumably a smaller percentage any younger. Hopefully, though, that’s changing.

So where do you sit in all of these stages of financial independence? Where would you like to be? What would best reflect your financial goals? I’d love to hear about them.

In the vein of sharing (and because we all love a little nosey into someone else’s stage), hubster and I are getting closer and closer to Stage 4. With the compounding benefits of our investments (that lovely interest on the principal sum as well as the accumulated interest already earned), will hopefully reach Stage 6 within the next decade.

Now, wouldn’t that be a nice place to exit stage left?

Leave a Reply

Want to join the discussion?Feel free to contribute!